2021 Forward Pricing & Pool Update

After beginning April at a spot value of 14.77 US cents per pound sugar sustained a rally for most of the period, peaking at 18.14 c/lb on the 12th of May.

During the past 6 weeks MSF has filled a significant volume of grower orders via the 2021 season Individual Forward Pricing Pool and Rolling Individual Forward Pricing Pool with an average hedged value of $472 per metric tonne actual.

- The highest 2021 MSF forward price filled to date for the 2021 season was $500 per metric tonne actual on the 7th of May.

- 2022 prices have also shown improvement with orders up to and including $450 filling on the 13th of May.

MSF’s latest pool numbers are below.

Major Headlines

What a month and a half it has been for the sugar market! The explanation behind the recent rally appears to have been a tale in two parts.

Firstly, commodities in general have rallied to their strongest level since 2011 as virus vaccinations, increased travel and roll out of vast economic stimulus by the worlds governments has resulted in boom demand for raw materials. Fears of inflation has also added to the strength of commodities which are a natural hedge to inflation.

Through the month of April most commodities, agricultural, metals and energy, recorded good gains with some of the strongest being: wheat +20%, coffee +17%, Sugar +20%, Corn + 30%, Copper +12%, Aluminium +10%, Nickel +10%, Brent Crude +7%, ethanol +23%.

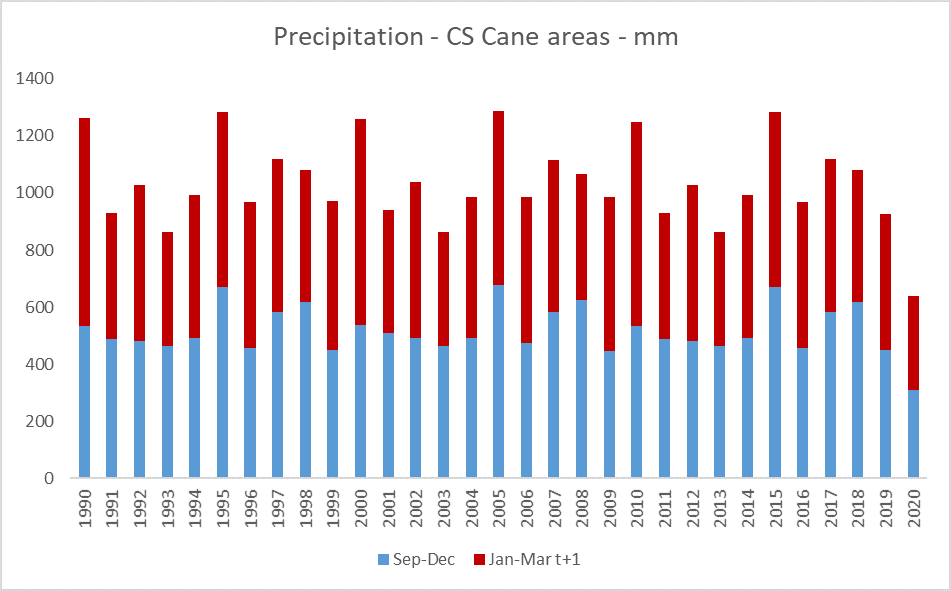

The second part to the recent rally has undoubtedly been Brazil and more specifically conjecture around the size of the crop which commenced harvesting in April. Major sugar traders Wilmar and Czarnikow released updates in late April painting Brazil’s sugarcane crop as a disaster due to ongoing dryness across the region. Below is a graph of September-March rainfall in Centre South Brazil going back to 1990 which does show a significant drop in rainfall during the crop development period.

Brazilian sugar industry group UNICA released its latest fortnightly crushing results on the 12th of May for the second half of April. Cane crushed, sugar and ethanol production for this period compared to the same period last year was significantly lower as only 205 mills were crushing as at 30 April 2021 compared to 217 last year. In terms of cane yield the average to date is 79.8 tonnes per hectare which is a 10% drop on 2020. This would appear significant however only a small sample of mills provided yield data and first round results can be misleading as we know.

Elsewhere the world remains largely unchanged, India has nearly exported it’s 6 million tonnes of sugar covered by the government export quota. At these prices it’s likely India will carry on exporting excess sugar stock without a subsidy once the quota is exceeded.

Thailand is in its inter-crop period with satisfactory rainfall to date. Thailand is focussing on expanding area under cane after a dismal 2020/21 harvest result of only 66 million tonnes of cane (compared to 130 million tonnes in 2018). Other crops have grown in popularity in Thailand, with values for most agricultural commodities experiencing a boom it may be a difficult task to bring Thailand back to 100+ million tonnes of cane quickly.

The AUD has traded around 0.77 with the USD for much of the past month having increased above 0.78 in recent days on the back of poor jobs data out of the United States.